Study

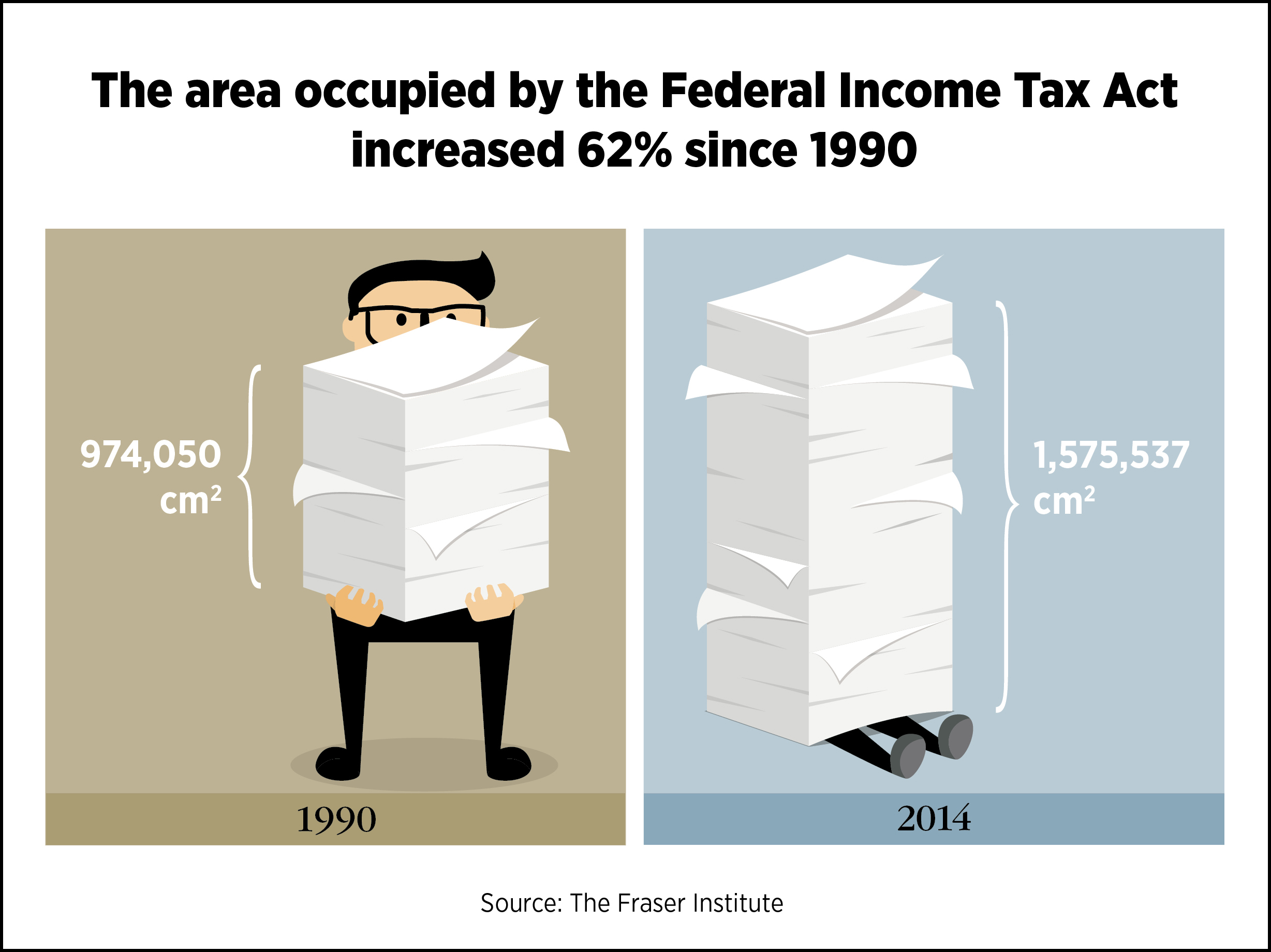

| EST. READ TIME 2 MIN.With the income tax deadline looming, Canadians challenged by an increasingly complex tax system

-

François Vaillancourt

François Vaillancourt is an emeritus professor in the department of economic sciences at the University of Montreal where he taughtfrom 1976 to 2011. He completed his Ph.D. in economics at Queen’s University in 1978 and received a Doctorate honoris causa from the University of Geneva in 2021 for his pioneering work in the economics of language. Professor Vaillancourt was a Fulbright scholar in 2007 in Atlanta and was elected to the Royal Society of Canada in 2009. He was the Shastri lecturer in India has been a guest lecturer at the University of Toronto and Australian National University and a research scholar at the Institute for Research in Public Policy (1992-2000) and the C.D. Howe Institute (2000-2003). Professor Vaillancourt was also a research coordinator(Income distribution and Income security) for the MacDonald Commission (1983-1986). He has consulted for a number of international organizations such as the IMF, the World Bank, OECD, UNDP and national agencies such as Statistics Canada, Finance Canada, and the Seguin Commission. His fields of research include linguistic policies, intergovernmental financial relations, and tax compliance costs. He has published on a wide variety of issues including equalization in federal countries, education, minority language policies, federalism, and taxation. Professor Vaillancourt is widely acknowledged as one of the pre-eminent scholars on the issue of tax compliance and administrative costs.… Read more -

Charles Lammam

-

Marylène Roy

Research Assistant, CIRANOMarylène Roy holds a BSc (Econ) from Université de Montréal and is currently studying for a MSc at HEC Montréal. She is a research assistant at CIRANO.