Études de Recherche sm

Les écoles secondaires du Québec montrent des signes d’amélioration partout dans la province

By: Yanick Labrie, Peter Cowley, Joel Emes and Max Shang

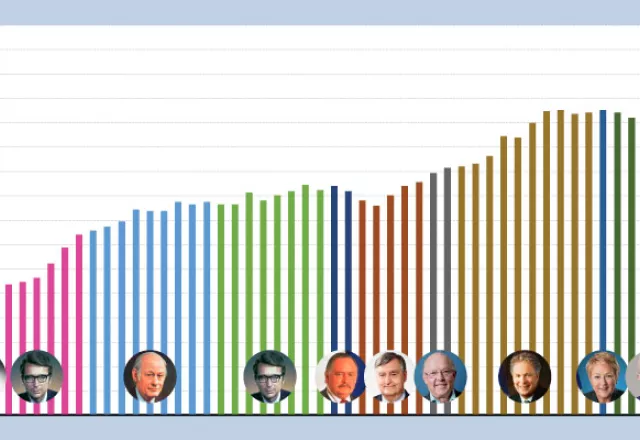

Les dépenses du gouvernement du Québec ont atteint le niveau le plus élevé jamais enregistré en 2021 à 15 562 $ par personne

By: Tegan Hill, Yanick Labrie and Hani Wannamaker

Les écoles secondaires du Québec montrent des signes d’amélioration partout dans la province

By: Yanick Labrie, Peter Cowley and Joel Emes

Le gouvernement du Québec a dépensé près de 80 milliards de dollars en subvention aux entreprises de 2007 à 2019

By: Tegan Hill and Joel Emes

Les travailleurs du secteur public au Québec reçoivent en moyenne des salaires 7,8 % plus élevés que les travailleurs comparables du se...

By: Milagros Palacios, Nathaniel Li and Ben Eisen

Les familles du Québec qui gagnent 100 000 $ ou plus font face aux taux d’imposition les plus élevés

By: Alex Whalen, Ben Eisen and Nathaniel Li

Les écoles secondaires du Québec montrent des signes d’amélioration partout dans la province

By: Yanick Labrie and Joel Emes

Les écoles secondaires du Québec montrent des signes d’amélioration partout dans la province

By: Yanick Labrie, Peter Cowley, Joel Emes and Max Shang

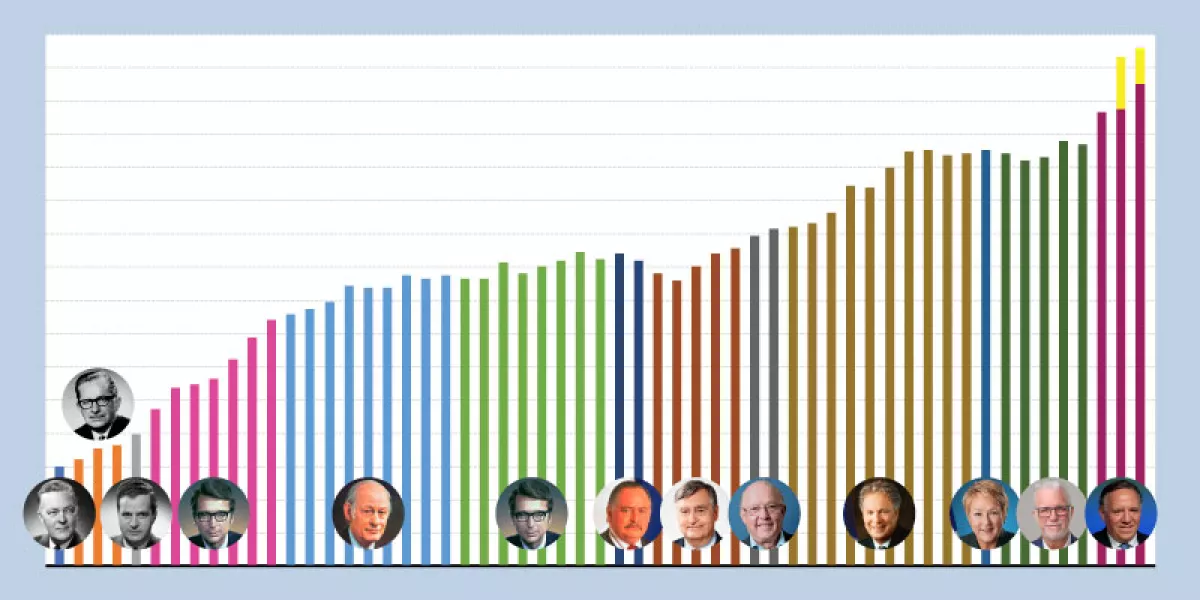

Les dépenses du gouvernement du Québec ont atteint le niveau le plus élevé jamais enregistré en 2021 à 15 562 $ par personne

By: Tegan Hill, Yanick Labrie and Hani Wannamaker

Les écoles secondaires du Québec montrent des signes d’amélioration partout dans la province

By: Yanick Labrie, Peter Cowley and Joel Emes

Le gouvernement du Québec a dépensé près de 80 milliards de dollars en subvention aux entreprises de 2007 à 2019

By: Tegan Hill and Joel Emes

Les travailleurs du secteur public au Québec reçoivent en moyenne des salaires 7,8 % plus élevés que les travailleurs comparables du se...

By: Milagros Palacios, Nathaniel Li and Ben Eisen

Les familles du Québec qui gagnent 100 000 $ ou plus font face aux taux d’imposition les plus élevés

By: Alex Whalen, Ben Eisen and Nathaniel Li

Les écoles secondaires du Québec montrent des signes d’amélioration partout dans la province

By: Yanick Labrie and Joel Emes

Commentaires

L’offre et la demande de logements au Québec: un équilibre menacé

By: Josef Filipowicz and Yanick Labrie

Délais d’attente en chirurgie—préparons l’après-pandémie

By: Yanick Labrie

Appeared in the Paru dans La Presse

Quand devons-nous nous soucier de la paie des PDG?

By: Vincent Geloso

Appeared in the Appeared in La Presse

Hongkong: La liberté économique ne garantit pas la liberté politique

By: Tanja Porčnik

Appeared in the Paru dans Le Figaro

Le 21 juin, vous travaillerez enfin pour vous!

By: Yanick Labrie

Appeared in the Paru dans le Journal de Montreal

Assainir les finances du Québec par un meilleur contrôle des salaires dans le secteur public

By: Charles Lammam

Appeared in the Paru dans La Presse

Dix milliards de bonnes raisons de réduire notre dette publique

By: Charles Lammam and Yanick Labrie

Appeared in the Paru dans La Presse

Le Bulletin des écoles secondaires sert bien le système d’éducation

By: Yanick Labrie

Appeared in the Paru dans Le Soleil

Les écoles indépendantes au Québec vont à l'encontre de la caricature «élitiste»

By: Yanick Labrie and Sazid Hasan

Appeared in the Paru dans La Presse

L’offre et la demande de logements au Québec: un équilibre menacé

By: Josef Filipowicz and Yanick Labrie

Délais d’attente en chirurgie—préparons l’après-pandémie

By: Yanick Labrie

Appeared in the Paru dans La Presse

Quand devons-nous nous soucier de la paie des PDG?

By: Vincent Geloso

Appeared in the Appeared in La Presse

Hongkong: La liberté économique ne garantit pas la liberté politique

By: Tanja Porčnik

Appeared in the Paru dans Le Figaro

Contactez-nous

Soutenez Notre Travail

L’Institut Fraser n’accepte aucun financement gouvernemental pour mener ses recherches. Il maintient son impartialité en s’appuyant sur ses partisans – des gens comme vous! Si vous soutenez le travail que nous faisons et souhaitez contribuer à le faire connaître à encore plus de Canadiens, pensez à faire un don dès aujourd’hui.