Study

| EST. READ TIME 4 MIN.Even modest interest rate hikes could endanger Ontario government’s promise of a balanced budget

An important fact to consider when assessing the medium-term fiscal plans announced by the federal and provincial governments is that interest rates are at historically low levels. A return to more normal levels would jeopardize promises for balanced budgets or surpluses and increase the proportion of revenues spent on debt interest payments (the “interest bite”). More revenue going to interest payments on the debt means less is available for programs that taxpayers value, such as health care and education, or tax relief.

This study analyzes the budgetary implications of interest rate risks faced by governments, using as examples the short- and medium-term budget plans (2016–17 to 2019–20) of Ontario and Quebec, Canada’s two largest provinces and the most indebted as a share of GDP. The study also provides a background discussion about interest rates and provincial debt maturity structures.

Two scenarios are considered where interest rates rise faster and/or higher than forecasted in Ontario’s 2015 budget. In Scenario 1, rates rise to 3.5 percent in 2016–17 and to 4.5 percent from 2017–18 to 2019–20. This compares to rates in the baseline case of 2.7 percent in 2016–17, 3.8 percent in 2017–18, 4.2 percent in 2018–19, and 4.5 percent in 2019–20. In Scenario 2, rates rise to 4.5 percent in 2016–17 and attain 5.0 percent from 2017–18 to 2019–20. (Quebec states its interest rate forecast only for 2016–17, but it projects its spending and revenues until 2019–20. The analysis assumes Quebec’s budget is based on the same interest rates as Ontario after 2016–17. While Ontario provides its medium-term interest rate forecast, it projects spending and revenues only to 2017–18. Hence, the analysis extends Ontario’s budget projections to 2019–20 by assuming that program spending and revenues will grow at the same rate as the economy.)

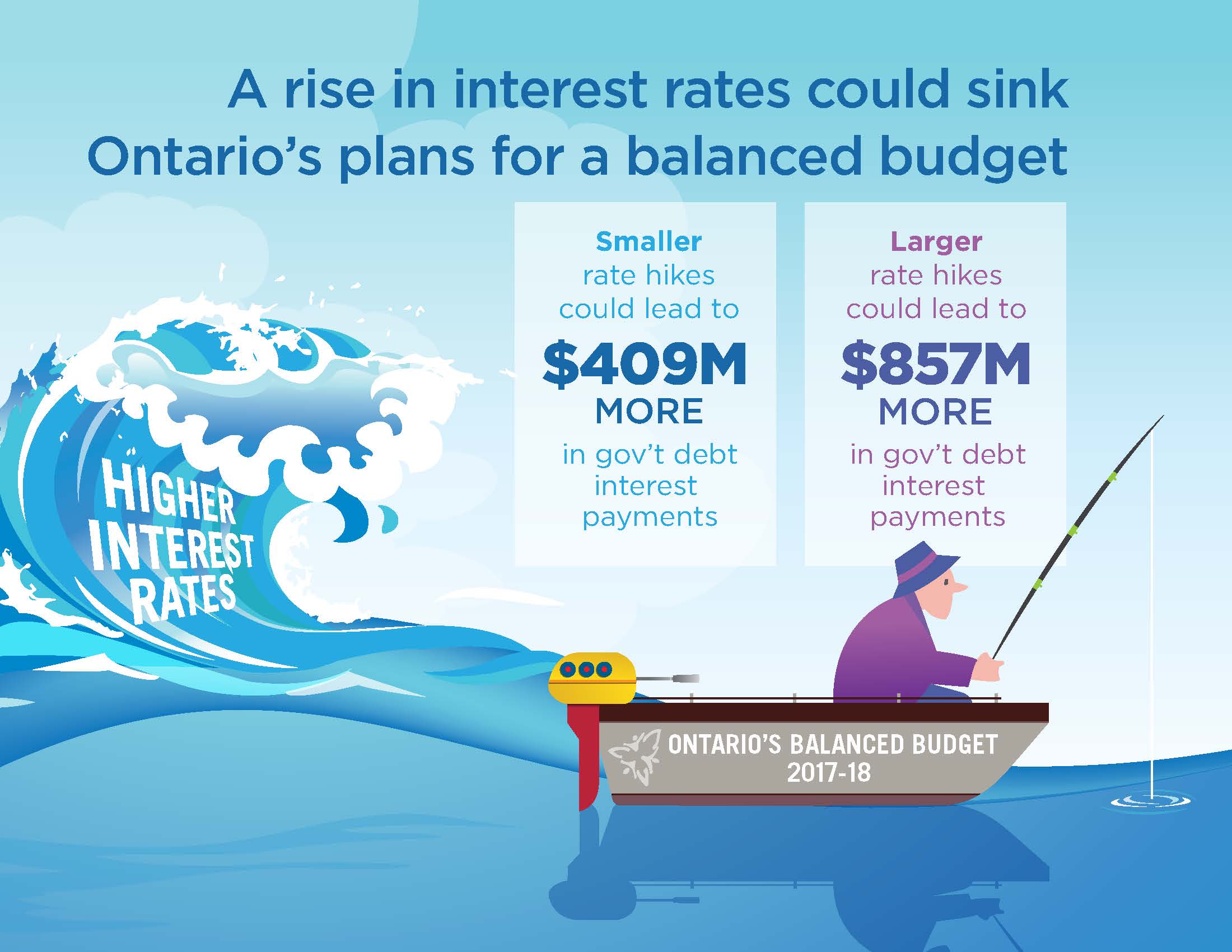

The interest rate shocks described by Scenario 1 would increase Ontario’s projected deficit by $264 million in 2016–17 and derail the government’s expectation of achieving budgetary balance in 2017–18. In Scenario 2, Ontario’s deficit increases by $616 million in 2016–17 and the expected budget balance in 2017–18 is replaced by a deficit of $857 million. In 2019–20, Ontario’s cost of interest rises by $498 million in Scenario 1 and to almost $1.2 billion in Scenario 2. Ontario’s interest bite would rise from its current value of 9.2 percent of revenues in 2015–16 to 10.1 or 10.4 percent in 2017–18 under Scenarios 1 and 2, respectively.

The Quebec government is projecting budget surpluses every year from 2016–17 to 2019–20. The effect of the interest rate shocks is to substantially reduce, though not reverse, the projected surpluses. Under Scenario 1, the surplus falls by $363 million in 2016–17 and by $440 million in 2019–20. In Scenario 2, Quebec’s projected surplus declines by $524 million in 2016–17 and by nearly $1 billion in 2019–20. Quebec’s interest bite would rise from its current value of 10.5 percent in 2015–16 to 10.8 or 11.3 percent in 2017–18 under Scenarios 1 and 2, respect¬ively. Thus, even relatively modest increases in interest rates would have important adverse effects on the short- and medium-term budgets of Ontario and Quebec, and would oblige the provinces to devote a larger share of revenues to financing interest payments on debt.

Provincial governments have been shifting the structure of their debts toward longer terms to maturity. In this way, they are able to postpone the need to refinance their debts at higher interest rates, if rates were to rise. However, in the long run all of the government’s debt eventually matures. The final part of the study explores the budgetary implications of interest rates on provincial debt ris¬ing to 5 percent permanently (with 2 percent price inflation), starting in 2016–17. The primary surplus (revenues minus non-interest spending) would have to be increased each year (forever) by about $3.5 billion in Ontario and by $2.1 billion in Quebec. Otherwise, provincial debt as a share of the economy would rise above the 2016–17 level in each province.

The analysis indicates that a faster-than-expected rise in interest rates toward normal levels could upset Ontario’s already delicate path toward fiscal sustain¬ability. In Quebec, the danger is mitigated to some extent by the government’s commitment to fiscal reforms, announced in its latest budget, to achieve annual surpluses through spending restraint. Should the government waver on its com¬mitment, then the interest rate risk would exacerbate the province’s already very high debt-to-GDP ratio. The bottom line is that governments should not be san¬guine about the current low interest rates when forming their upcoming budgets.

-

Jean-François Wen

Jean-François Wen is a Professor of Economics and a Research Fellow at the School of Public Policy at the Universityof Calgary. He has published articles in leading journals on the effects of taxation and social insurance programs on economic performance and income inequality. He is a co-author of the textbook Public Finance in Canada and has served as a consultant for the World Bank and the International Monetary Fund concerning policy reforms in various countries. Most recently, he co-authored a report on tax reform in Gabon that served as the basis of a workshop with government officials and privatesector representatives held last year in Libreville.Professor Wen was previously a faculty member of the School of Business and Economics at Wilfrid Laurier University and an economist at the Bank of Canada. He has a Ph.D. from Queens University and holds the Chartered Financial Analyst (CFA) designation.… Read more