Study

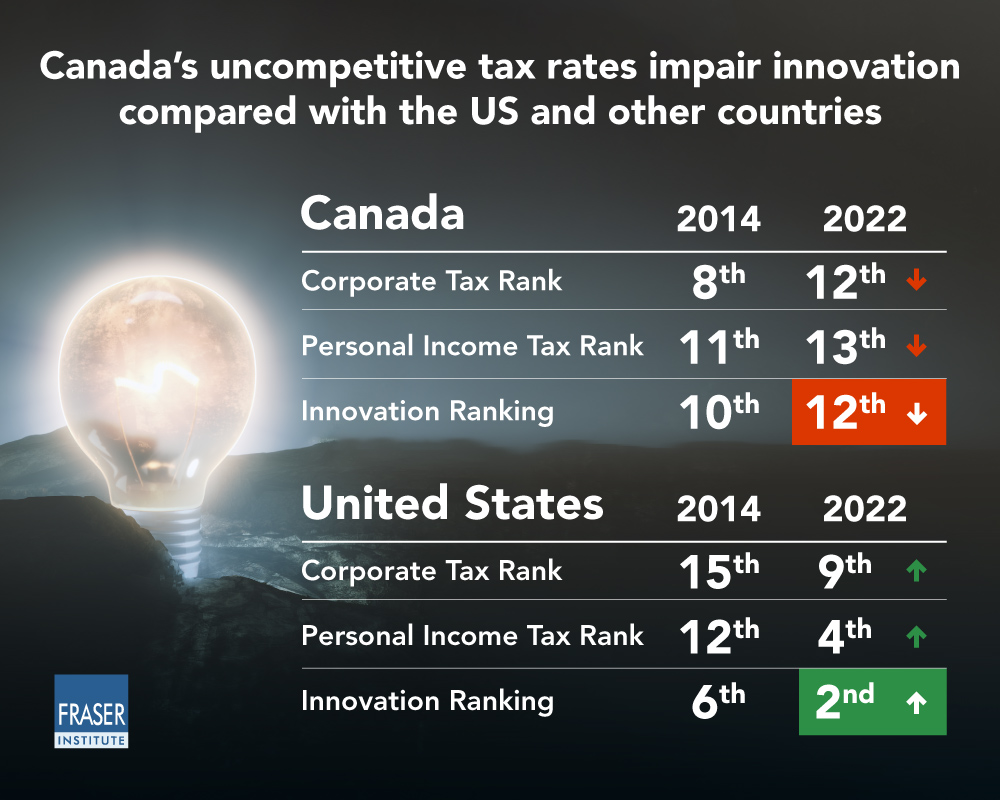

| EST. READ TIME 4 MIN.Canada fell to 12th position in global innovation rankings over past decade, while U.S. improved to 2nd

Taxes, Innovation, and Productivity Growth

The relationship between a nation’s tax policy and its standard of living has been a longstanding topic of debate. While many economists and policy analysts argue that higher taxes discourage real economic growth, others reject the argument or claim that taxes are a relatively unimportant influence on standards of living compared to other determinants such as physical infrastructure.

Empirical studies document the critical role that technological change plays in improving the productivity of labour and capital, while improved productivity underlies increases in the real incomes of domestic factors of production. Technological change is broadly equivalent to innovation, where the latter can be thought of as the creation, introduction, and widespread commercial use of new knowledge that takes the form of new products, new production and distribution techniques, and new ways of organizing production and distribution activities.

Innovation is the main underlying contributor to improved total factor productivity (TFP) and, therefore, to higher standards of living. Hence, the influence of tax policy on the quantity and quality of innovation activity is an important public policy issue.

Tax policy encompasses the economic activities and payments to factors of production that are subject to taxation, the tax rates that are applied, particularly the progressivity of the relevant tax schedule, and the exemptions, deductions, and credits that are applicable to specific activities or sources of income.

Innovation activities are inherently risky and will be undertaken by private sector organizations only if the expected risk-adjusted returns from the relevant investments exceed the costs of capital for those organizations. Likewise, individuals involved in the innovation process, such as scientists and engineers, will invest in education and other training needed to participate effectively in innovation activities only if the expected returns to the necessary investments in human capital exceed the associated costs.

For all private sector organizations and individual entrepreneurs, scientists, and other participants in innovation activities, the relevant payoffs are net of taxes. Hence, a relatively straightforward insight is that higher taxes will discourage innovation, at the margin. However, the magnitude of the relationship between taxes and innovation is an empirical issue. A related empirical issue is whether tax credits for activities such as research and development (R&D) are more effective at promoting innovation than reductions in general corporate and personal income taxes.

This essay reviews the relevant literature and documents the negative effect that higher corporate and personal income taxes have on innovation, where the latter is most typically measured by patenting activity. Entrepreneurship, as typically measured by business start-ups, is a less frequently used measure of innovation whose link to taxes has also been studied. As in the case of patenting, higher corporate and personal income taxes are found to discourage innovation, although the empirical relationship is not as strong as it is when patenting is used as the measure of innovation. Also, the effect of tax increases on innovation appears to be stronger than that of tax decreases. The strongest impact of innovation seems to come from marginal tax rate increases on high-income earners.

Companies and high-income earners, where the latter include “star” scientists, are geographically mobile. Hence, increasing marginal tax rates in specific geographical jurisdictions will reduce innovation activities in those jurisdictions by encouraging out-migration of companies and star scientists to jurisdictions with lower marginal tax rates.

Empirical studies also show that R&D tax credits and direct government grants for innovation activities do encourage increased R&D spending and other investments in innovation, at the margin. However, governments, including the Canadian government, typically target R&D tax credits and grants to small and medium-sized firms that produce fewer innovations per dollar of R&D spending than larger firms. In addition, R&D is only one activity in the chain of activities contributing to technological change. Hence, tax credits and grants aimed at promoting R&D do not address incentives to commercialize the new knowledge created by R&D, while government subsidies to promote innovation activities more broadly involve bureaucrats choosing the firms and industrial sectors that will be subsidized, which is less efficient than having capital markets determine the allocation of funding for innovation.

Canada has had an undistinguished record of innovation performance compared to other advanced economies. Its relatively poor performance in innovation is consistent with its uncompetitive tax environment. The Tax Foundation identifies Canada as having relatively uncompetitive corporate and personal income tax environments compared to other wealthy countries that rank higher in innovation performance. Of particular concern is the decline in Canada’s tax competitiveness ranking relative to that of the US in recent years. Given the substantial cross-border migration of highly educated individuals between Canada and the US, as well as the large amount of cross-border corporate investment, a less attractive tax environment in Canada relative to the US is a significant potential handicap to increased innovation in Canada.

-

Steven Globerman

Senior Fellow and Addington Chair in Measurement, Fraser Institute

Mr. Steven Globerman is a Senior Fellow and Addington Chair in Measurement at the Fraser Institute. Previously, he held tenuredappointments at Simon Fraser University and York University and has been a visiting professor at the University of California, University of British Columbia, Stockholm School of Economics, Copenhagen School of Business, and the Helsinki School of Economics.He has published more than 200 articles and monographs and is the author of the book The Impacts of 9/11 on Canada-U.S. Trade as well as a textbook on international business management. In the early 1990s, he was responsible for coordinating Fraser Institute research on the North American Free Trade Agreement.In addition, Mr. Globerman has served as a researcher for two Canadian Royal Commissions on the economy as well as a research advisor to Investment Canada on the subject of foreign direct investment. He has also hosted management seminars for policymakers across North America and Asia.Mr. Globerman was a founding member of the Association for Cultural Economics and is currently a member of the American and Canadian Economics Associations, the Academy of International Business, and the Academy of Management.He earned his BA in economics from Brooklyn College, his MA from the University of California, Los Angeles, and his PhD from New York University.… Read more