Study

| EST. READ TIME 2 MIN.Reducing Ontario’s personal and corporate income tax rates to 8% would attract investment, top talent

Time for Tax Reform in Ontario

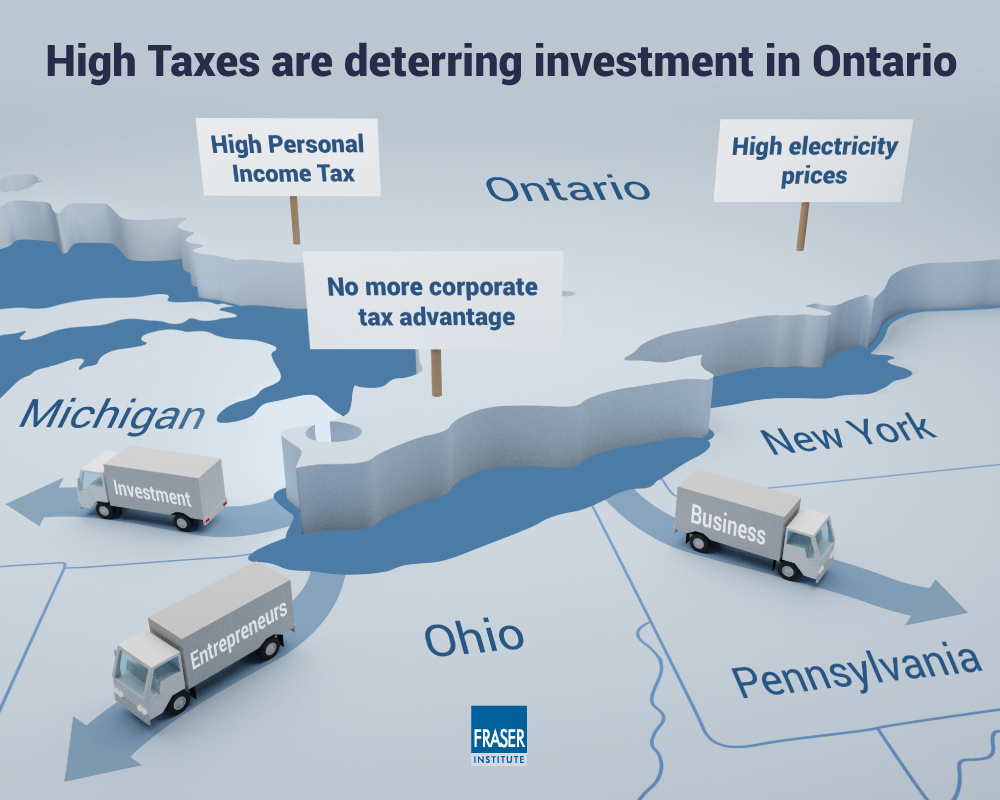

Over the past fifteen years, Ontario’s provincial economy has struggled relative to the rest of the country. The reasons for Ontario’s economic weakness are complex and varied. However, public policy choices have been a contributing factor.

One area that stands out as a particularly strong candidate for reform is tax policy. Specifically, Ontario’s personal income tax (PIT) system undermines Ontario’s economic competitiveness and therefore hinders economic growth. With seven brackets and high marginal rates, Ontario’s PIT discourages a wide range of productive activities and makes it more difficult for Ontario to retain and attract higher-earning individuals. These problems are compounded by the fact that Ontario’s PIT is not competitive with peer jurisdictions in North America. Ontario has the second highest top marginal PIT rate in North America (combined federal/provincial or federal/state) at 53.53 percent.

This study presents an outline for tax reform in Ontario which would transform the province’s uncompetitive PIT system, while also reducing the province’s Corporate Income Tax (CIT) to make Ontario a more attractive destination for investment and entrepreneurship.

The paper examines the status quo in Ontario, and Ontario’s competitiveness in a North American context when it comes to both personal and corporate income taxes. Specifically, we show that Ontario’s PIT system is uncompetitive in the North American context, while the once strong corporate income tax advantage Ontario until recently enjoyed compared to the United States has for the most part disappeared.

The paper also describes an outline for policy reform, which includes replacing Ontario’s seven-bracket PIT system with a single-rate PIT in which all taxable income is taxed at a rate of 8 percent. The reform outline presented here also would lower the CIT from 11.5 percent to 8 percent.

Taken together, the PIT and CIT reforms outlined in this paper would create an important advantage for Ontario’s economy by making the province one of the most attractive tax jurisdictions in North America with respect to the taxation of both personal and corporate income. As a result, these changes would help create an economic environment in which businesses, entrepreneurs, and other skilled workers are better incentivized to work, invest, and create opportunities.

With new competitiveness pressures emerging from the United States, the advantages of policy reforms that make Ontario more attractive for investment and human capital are particularly pronounced at this moment in history.

-

Ben Eisen

Senior Fellow, Fraser Institute

Ben Eisen is a Senior Fellow in Fiscal and Provincial Prosperity Studies and former Director of Provincial Prosperity Studies at theFraser Institute. He holds a BA from the University of Toronto and an MPP from the University of Toronto’s School of Public Policy and Governance. Prior to joining the Fraser Institute Mr. Eisen was the Director of Research and Programmes at the Atlantic Institute for Market Studies in Halifax. He also worked for the Citizens Budget Commission in New York City, and in Winnipeg as the Assistant Research Director for the Frontier Centre for Public Policy. Mr. Eisen has published influential studies on several policy topics, including intergovernmental relations, public finance, and higher education policy. He has been widely quoted in major newspapers including the National Post, Chronicle Herald, Winnipeg Free Press and Calgary Herald.… Read more -

Steve Lafleur

Steve Lafleur is a research director at the Institute for Research on Public Policy, a former senior fellow of theFraser Institute and a former senior policy analyst at the Fraser Institute. He holds an M.A. in Political Science from Wilfrid Laurier University and a B.A. from Laurentian University where he studied Political Science and Economics. He was previously a Senior Policy Analyst with the Frontier Centre for Public Policy in Winnipeg and is a Contributing Editor to New Geography. His past work has focused primarily on housing, transportation, local government and inter-governmental fiscal relations. His current focus is on economic competitiveness of jurisdictions in the Prairie provinces. His writing has appeared in every major national and regional Canadian newspaper and his work has been cited by many sources including the Partnership for a New American Economy and the Reason Foundation.… Read more -

Joel Emes

Senior Economist, Fraser InstituteJoel Emes is a Senior Economist, Addington Centre for Measurement, at the Fraser Institute. Joel started his career with theFraser Institute and rejoined after a stint as a senior analyst, acting executive director and then senior advisor to British Columbia’s provincial government. Joel initiated and led several flagship projects in the areas of tax freedom and government performance, spending, debt, and unfunded liabilities. He supports many projects at the Institute in areas such as investment, equalization, school performance and fiscal policy. Joel holds a B.A. and an M.A. in economics from Simon Fraser University.… Read more