Major changes to Canada’s federal personal income tax—1917-2017

As a result of the funding demands of the First World War, Canada’s federal government introduced both a personal and corporate income tax in 1917. The advent of the personal income tax in particular marked a significant shift in federal taxation philosophy.

In the first years of Confederation, it was felt that taxing incomes would detract from Canada’s competitive position as one of the lowest taxed countries in the world. Indeed, it’s worth noting that Canada’s federal personal income tax only came into being once the United States brought in its own income tax in 1913. This post highlights some of the major changes to the federal personal income tax in its first 100 years.

Canada’s federal personal income tax came into effect September 20, 1917 with a 4 per cent tax on all income of single people (unmarried persons and widows or widowers without dependent children) over $2,000. For everyone else, the personal exemption was $3,000. In today’s dollars, the exemptions would be worth approximately $33,000 and $50,000, respectively. To be clear, in today’s dollars, the first federal personal income tax exempted the first $33,000 of income for single people and the first $50,000 for everyone else. For reference, the basic personal exemption for 2016 is $11,474.

For married Canadians with dependents and an annual income greater than $6,000 (roughly $99,500 in today’s dollars), the tax rate ranged from 2 to 22 per cent. However, because of the relatively high dollar exemptions, only between 2 and 8 per cent of individuals had to file tax returns during the initial years of the federal personal income tax.

It was the Second World War that saw the federal personal income tax expand dramatically. There was a flat 20 per cent surtax imposed on all income tax payable by persons other than corporations in 1939 followed by the introduction of a new tax on income known as the National Defence Tax. Further rate increases along with reduced exemptions were introduced in 1942.

Perhaps the most notable of these changes was the introduction of high marginal tax rates. For example, the pre-Second World War marginal tax rate on taxable income between $1,000 and $2,000 in the dollars of the day was 4 per cent. By 1942, it had increased to 44 per cent. For taxable income between $10,000 and $15,000 it was 13.7 per cent before the war, but fully 69 per cent by 1942.

While these rates came down after the war, they remained substantially higher than they had been before the war. By 1971, for instance, the average Canadian was subject to much higher average and marginal tax rates than had been the case in 1946.

Moreover, the proportion of the population having to file income taxes rose and then continued to rise in the post-war era. In 1938, for instance, only 2.3 per cent of the population filed personal income taxes, whereas by 1955 24 per cent of the population did. By 1975 that number had grown to 52 per cent and it reached 68 per cent by the early 1990s. At present, approximately 75 per cent of Canadians file a personal income tax return. Many Canadians who don’t actually pay income taxes have an incentive to file in order to qualify for refundable tax credits, such as the GST credit.

Figure 1 presents the inflation-adjusted (in 2016 dollars) total personal income tax revenue for the federal government. In 1918, total revenue (in real dollars) from the federal personal income tax amounted to $116 million whereas by 2017 it’s expected to total $150.7 billion. Interestingly, as evidenced by the data in Figure 1, the real increases in federal personal income tax revenues don’t begin until roughly the mid-1960s, though the foundation for those increases was established during the Second World War.

In terms of per-person federal personal income taxes, the burden has increased from roughly $14 per person in 1918 (adjusted for inflation and denoted in 2016 dollars) to roughly $4,120 in 2017, an almost 300-fold increase.

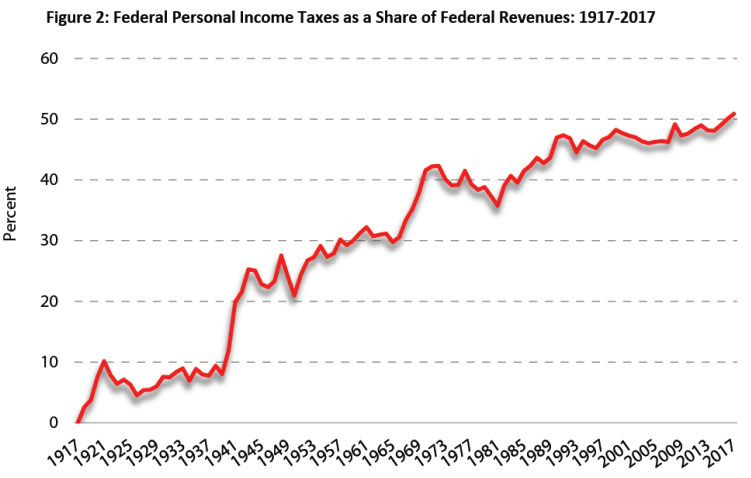

After a century of changing brackets, rates and exemptions, along with periodic reforms designed to broaden the base and lower the rates, the importance of the federal personal income tax as a revenue source has steadily grown as Figures 2 and 3 illustrate. As a share of total federal revenue, the personal income tax has grown from 2.6 per cent of revenue in 1918 to an expected 51 per cent in 2017. Large increases in the share of federal revenues represented by personal income taxes are evident at the beginning of the Second World War and the late 1960s, though a steady increase is generally observed across the entire 100-year history of the tax.

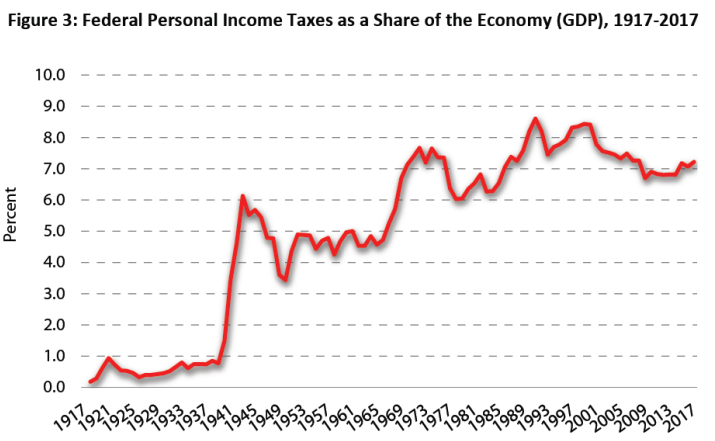

Similarly, as a share of the economy (GDP), federal PIT revenue has grown from 0.2 per cent in 1918 to an expected 7.2 per cent in 2017. The trend in personal income taxes as a share of the economy (Figure 3) is quite different than its share of federal revenues (Figure 2). For instance, we observe periods in Figure 3 where federal personal income taxes are declining as a share of the economy both due to economic circumstances such as recessions and/or through purposeful reductions in tax rates.

It’s ironic that a tax that was anathema to federal politicians during the first 50 years after Confederation, and that many believe was brought in and sold as a temporary wartime measure, has come to be the dominant source of federal government revenue. Indeed, both its creation and its most dramatic expansion occurred during periods of war. While the late 20th century saw a period of reform that resulted in a reduction in the number brackets, a lowering of rates and a broadening of the base, recent federal government revenue policy has taken the first steps towards both higher rates and more brackets.

Learn more about the history of Canada’s personal income tax here.

Author:

Subscribe to the Fraser Institute

Get the latest news from the Fraser Institute on the latest research studies, news and events.