Too many analyses misrepresent capital gains income and taxes

As the federal budget quickly approaches and rumours regarding a likely increase in capital gains taxes intensify, it’s worthwhile to consider how many of the analyses calling for higher capital gains taxes confuse capital gains income versus taxes.

As demonstrated in an earlier commentary, capital gains taxes have been shown both domestically and internationally to be a costly way to raise revenue because they impose significant economic costs on economies that use them while not raising much revenue. Put simply, they’re a high-cost way for governments to raise revenue.

The following section is taken from a 2014 essay by Charles Lammam and Jason Clemens along with former intern Matthew Lo. It explains why the equity argument often used to justify increasing capital gains, which is likely to be incorporated if indeed the federal government makes the unfortunate decision to increase the tax rate, is quite incorrect.

In spite of the clear economic costs associated with capital gains taxation, its proponents tend to support it on equity grounds. It’s frequently claimed that only a small percentage of high-income earners realize capital gains, and the perceived unequal distribution of capital gains has in effect become the primary argument against capital gains tax reductions. As a Standing Senate Committee report summarized in 2000:

…the arguments in favour of lowering the capital gains tax are primarily economic… The arguments against a significant reduction in the capital gains tax are based primarily on the grounds that the direct effect of such a reduction has a disproportionate impact on higher-income taxpayers.

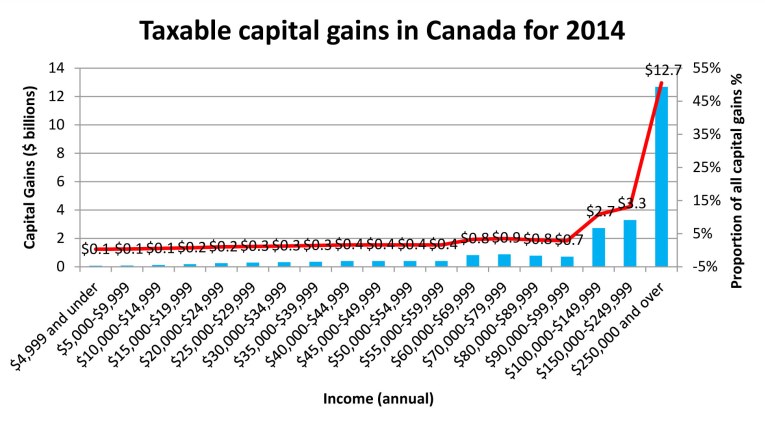

This equity argument against capital gains tax reductions has been advanced by researchers in Canada and elsewhere. Daniel Feenberg and Lawrence Summers, Jesper Roine and Daniel Waldenstrom, and Thomas Hungerford have studied the capital gains income distribution in different jurisdictions and concluded that the concentration of capital gains with a small percentage of high-income earners is a source of inequality and a justification for maintaining capital gains taxes. Jackson, Yalnizyan and Macdonald have reached similar conclusions about the income distribution of capital gains realizations in Canada and also argued for higher capital gains tax rates in order to offset the perceived inequity. Government data on taxable capital gains are often cited as evidence of unequal distribution. As per figure 1 below, income statistics provided by the Canada Revenue Agency for 2014 show that Canadians earning $250,000 or more reported 51 per cent of taxable capital gains.

There are problems with relying on tax data to evaluate the distribution of capital gains, however. The first issue is that a considerable percentage of Canadians earn capital gains in Tax-Free Savings Accounts (TFSAs), Registered Retirement Savings Plans (RRSPs), Registered Pension Plans (RPPs), and in their primary residences, but these capital gains are either non-taxable or treated as regular income and therefore are not reflected in the tax data as capital gains. The point is that government policy already exempts capital gains from taxation for a large share of taxpayers in the name of encouraging investment, savings and homeownership.

The TFSA was created in 2009 and allows for Canadians to contribute up to $5,500 annually in a tax-free account. Any capital gains or dividends earned in a TFSA are non-taxable and therefore do not show up in taxable capital gains data. According to the Canada Revenue Agency, approximately 11.7 million Canadians hold TSFAs with a total value of $152 billion in assets. In 2014, about 23 per cent of the total value in TFSA contributions was made by individuals with incomes between $20,000 and $40,000, and more than 16 per cent was made by individuals earning less than $20,000. If capital gains incurred in TFSAs were accounted for, the distribution of capital gains would likely be much less concentrated than suggested by the current tax data.

Further, RRSPs are tax-preferred individual accounts designed to help Canadians save for retirement. An individual’s contribution is tax deductible. Any capital gains incurred in an RRSP is exempt from taxation until funds are removed from the RRSP, and the capital gain is taxed as regular income. It means that any capital gains incurred in RRSPs are not reflected in the tax data.

This has implications for the income distribution of capital gains. In 2015, 6.0 million Canadians contributed to an RRSP and the value of contributions that year was $39.2 billion. In total, all assets held in individual RRSPs were valued at $1.1 trillion in 2015. It’s difficult to estimate the extent to which RRSPs holders are incurring capital gains in their respective accounts but it’s likely that some percentage is and these data are not reflected in taxable capital gains.

Finally, RPPs are employment-based pension plans that are based on employee and/or employer contributions. Any capital gains incurred in an RPP, like in RRSPs, is exempt from taxation until the income is distributed from the RRP, at which point the capital gains are taxed as regular income. This means that any capital gains incurred in RPPs are excluded from the tax data. This also likely has consequences for the income distribution of capital gains. According to Statistics Canada, 32 per cent of the labour force in Canada participated in some type of RPP in 2011. The total market value of all RPP assets in 2015 is $1.7 trillion.

In addition to TFSAs, RRSPs and RPPs, capital gains realized from the sale of an individual’s primary residence are not subject to taxation. The home ownership rate in Canada is now approximately 70 per cent—among the highest rates in the industrialized world. Any data on the distribution of capital gains resulting from the sale of an individual’s primary residence is excluded from the data on taxable capital gains.

The result is that a considerable percentage of capital gains income is earned in tax-sheltered vehicles. Indeed, an OECD study estimates that approximately 90 per cent of individuals will ultimately be able to hold all of their financial assets in tax-sheltered vehicles as the TFSA matures over time.

The second challenge with relying on tax data is that it includes taxable capital gains income in people’s annual income, which inflates an individual’s annual income due to one-time asset sales and contributes to the concentration of taxable capital gains among high-income earners. This method of presenting the income distribution of taxable capital gains therefore provides a flawed picture.

By presenting income levels net any taxable capital gains, this method overstates the income distribution by pushing those with large one-time capital gains into higher income groups. But these gains are often atypical and can create a misleading picture about the income levels of those who incur capital gains. For instance, the owners of a small business may have lower incomes and reinvest earnings back into their business to build up a nest egg for retirement. It will appear that in the tax year such people sell their business and retire they are high-income earners, even though it’s a one-time spike in their personal income. Put simply, the lumpy nature of asset dispositions results in statistics on the incomes of those with capital gains that tend to overstate their wealth.

A more appropriate measure of the distribution of taxable capital gains would be pre-taxable capital gains income. Herbert Grubel discussed in detail economist Joel Emes’ attempt to understand the extent to which the current method affected the income distribution of taxable capital gains. With data from Revenue Canada, Emes found that, in 1992, 78 per cent of capital gains taxes were paid by families with incomes above $100,000, and that only 8 per cent were paid by families with incomes below $50,000. Backing out capital gains income, however, changed the income distribution considerably. Using this method, Emes found that families with income above $100,000 paid 26.8 per cent of capital gains taxes and those with incomes below $50,000 paid 52.1 per cent of such taxes.

A similar analysis for 2010 finds a comparable distributional breakdown after accounting for pre- and post-taxable capital gain income.

Concern about the income distribution of capital gains ignores the fact that a significant number of Canadians across income scales realize capital gains even if these are not reflected in the tax data. Any debate about the equity of capital gains taxes therefore needs to account for this reality. Tax policy can sometimes involve important trade-offs between the principles of equity and economic efficiency and any debate about capital gains taxes should not overstate the potential equity concerns.

Authors:

Subscribe to the Fraser Institute

Get the latest news from the Fraser Institute on the latest research studies, news and events.